N.O.A.H's ARC - Naturally Occurring Affordable Housing

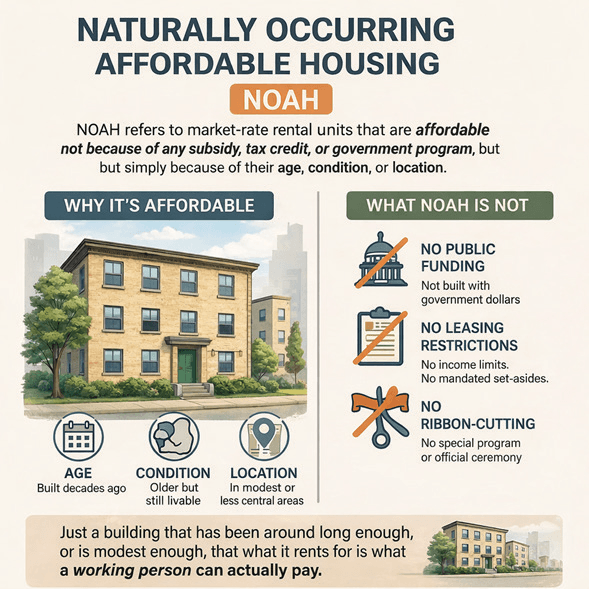

There is a term in housing policy, Naturally Occurring Affordable Housing, or NOAH, that most rental housing providers have probably never heard, even though it describes exactly what they provide to their communities.

How to know if you provide NOAH: If you own a 1972 fourplex. If you inherited a duplex from your parents. If you bought a house during the recession and kept it as a rental when you moved. If you manage a 40-unit walkup that was built when Gerald Ford was president. If working class folks can afford to live there, you are a NOAH provider. You are, statistically, America’s affordable housing infrastructure.

And almost nobody is talking about what happens when you can’t afford to keep doing it.

THE ARC

With limited exceptions, rental units in America follow the same trajectory. It starts by being expensive. A new apartment building opens with designer finishes, a fitness center, premium location, and asking rents north of $1,800. It attracts higher-income tenants. It has to.

Construction costs, land, and financing demand those rents. Often, new buildings open with introductory pricing or concessions, a free month or a waived deposit, to fill units quickly and pull tenants from older competitors. The downward pressure starts on day one.

Then time does what time does. The appliances age. The finishes go out of style. A newer building opens down the street with modern amenities like Tesla fast charging stations. A different part of town becomes trendy or closer to a better employer. The original building adjusts. Rents come down, or more often, they rise slower than inflation, which means they become more affordable in real terms even if the number on the lease stays flat. What was Class A becomes Class B, then Class C.

This is not failure. This is the mechanism. This is how market-rate housing becomes affordable housing: through age, through competition, through the natural lifecycle of a building. It is the single largest source of affordable rental housing in the United States, and it has never received a dime of federal subsidy to do it. And it works, when you let it.

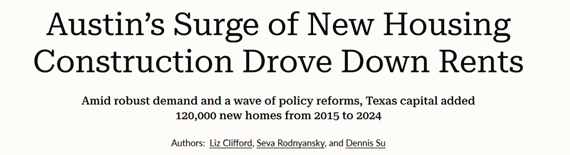

The Pew Charitable Trusts just published a case study on Austin, Texas, that demonstrates this arc in real time.

After a decade of zoning reforms and aggressive construction, 120,000 new homes from 2015 to 2024, Austin produced the steepest rent decline of any large U.S. metro. Rents in large apartment buildings fell 7 percent from 2023 to 2024. But here’s the number that matters: rents in Class C buildings, the older, non-luxury structures that house lower-income renters, fell 11.4 percent. Class A buildings, the new luxury product, fell only 2.6 percent.

The new supply didn’t just serve high-income renters. It competed with the existing stock, which competed with the stock below it, which drove down rents across the entire distribution. The biggest winners were the tenants in the oldest, most modest buildings. Nobody mandated those rent reductions. Nobody subsidized them. The arc did the work.

THE RENTERS

There is a persistent narrative that renting is a condition people are trapped in, that rental property providers are hoarding housing and forcing people to pay for something they would otherwise own. It’s a politically useful story. It also doesn’t survive contact with the data.

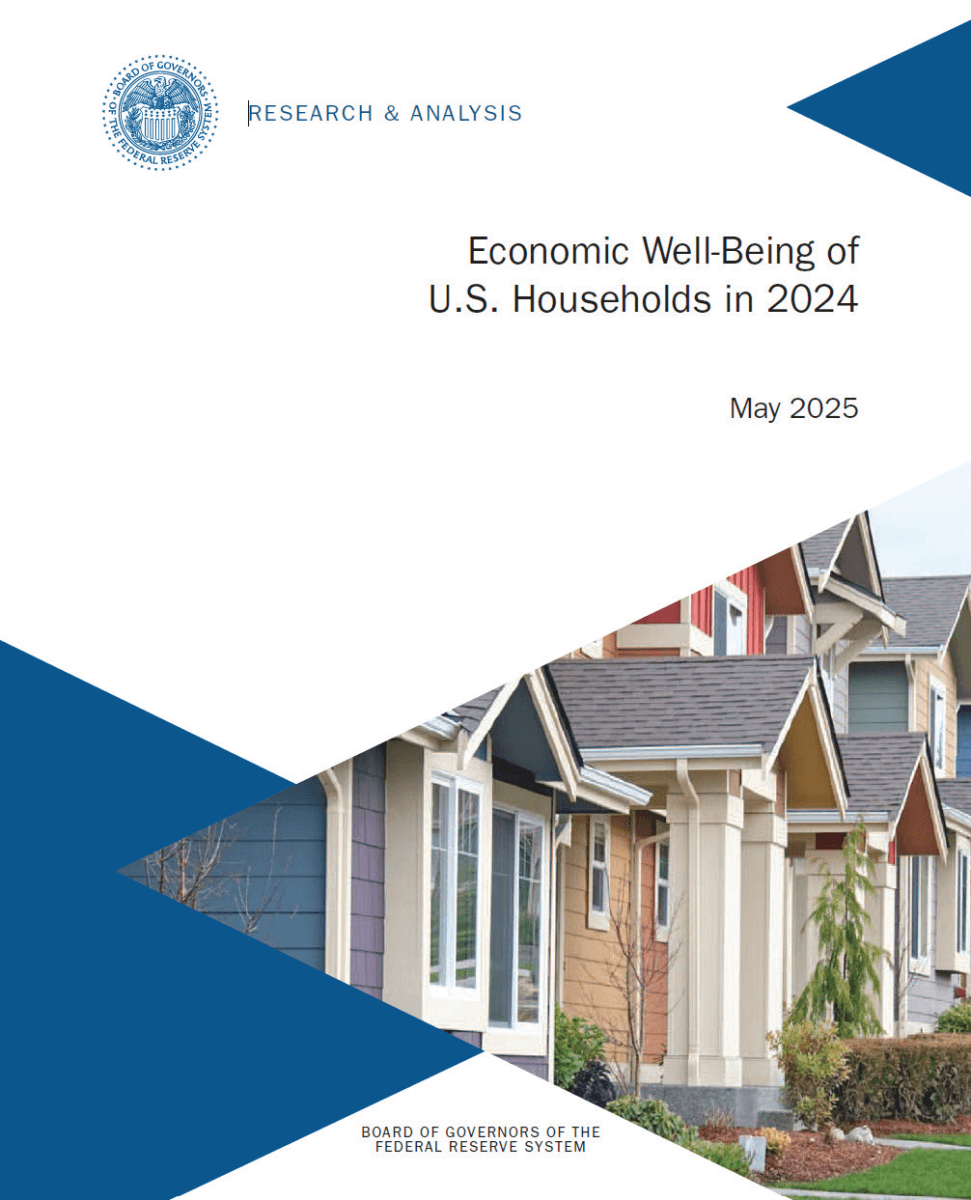

According to the Federal Reserve’s 2024 survey on the economic well-being of U.S. households, 58 percent of renters say renting is more convenient or flexible than owning. Only 39 percent said they prefer to rent long-term, which means the majority still view ownership as the ultimate goal, and rightfully so, as it remains the traditional engine for building generational wealth.

But interest, readiness, and demographic reality are colliding. People are marrying later. They are having children later in life, or not at all. The traditional single-family home was designed for a traditional family timeline that fewer Americans are actually following. Yet the cultural expectation, a deep-seated fear of missing out on the American Dream, remains. This creates a complex tension for today’s renter: the flexibility of renting is often the most rational, adaptable response to a mobile workforce and shifting family planning, even as the psychological desire for equity keeps ownership on a pedestal.

But interest, readiness, and demographic reality are colliding. People are marrying later. They are having children later in life, or not at all. The traditional single-family home was designed for a traditional family timeline that fewer Americans are actually following. Yet the cultural expectation, a deep-seated fear of missing out on the American Dream, remains. This creates a complex tension for today’s renter: the flexibility of renting is often the most rational, adaptable response to a mobile workforce and shifting family planning, even as the psychological desire for equity keeps ownership on a pedestal.

We also live in a world of radical transparency. Thirty years ago, you bought a house partly because you couldn’t see what else was out there. Now Zillow shows you every home for sale in every city. Indeed shows you every job. The result is something that looks a lot like paralysis by abundance. For many, renting is the rational response to a world with too many options to commit to one address permanently.

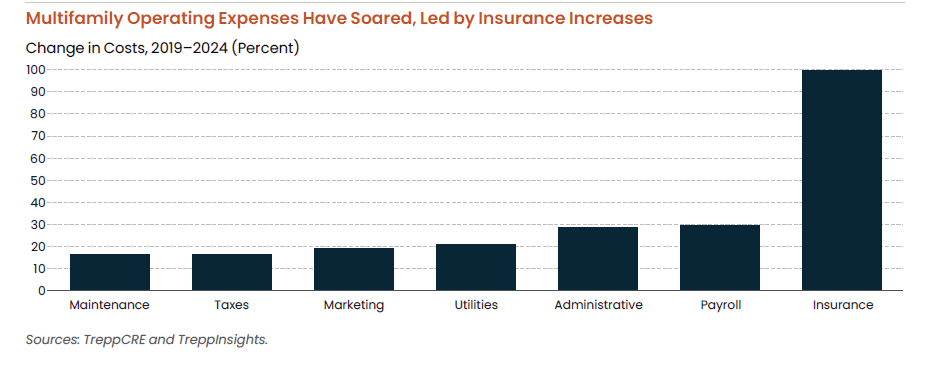

And here’s what the “hoarding” narrative conveniently ignores: every cost that makes renting expensive also makes owning expensive. While holding a deed eventually builds equity, it does not provide an escape hatch from the day-to-day carrying costs of property. Insurance premiums that doubled for apartment operators also doubled for homeowners. Material costs that rose 42 percent since 2020 apply to every roof, every furnace, every plumbing repair, whether the building is a rental or a residence. Property taxes don’t care about tenure. Labor costs don’t either.

When someone buys a home in this environment, they aren’t escaping those costs. They’re absorbing them directly, with their own savings, their own credit, and none of the economies of scale that even a small rental operator can sometimes access. Harvard reports that a household now needs more than $120,000 in income to afford the median-priced home. For many Americans, renting isn’t a trap. It’s the only math that works.

The real question isn’t why people rent. It’s who is going to keep providing the rental housing they need, at a price they can afford.

THE PROVIDERS

A significant share of the people operating America’s most affordable housing never set out to provide rentals at all.

They inherited a property. They couldn’t sell a house during a downturn and rented it instead. They bought a duplex because the mortgage math worked with a tenant paying half. They are teachers, electricians, retirees, and small business owners. They own one, two, maybe ten units. They operate on conservative margins, with cash reserves saved for routine and foreseen maintenance.

These providers own and operate nearly half of America’s rental stock. Single-family rentals are 31 percent of all rental units nationally. Small multifamily buildings add another 17 percent. That’s roughly 23 million units, the vast majority in the NOAH category.

The Harvard Joint Center for Housing Studies, one of the most respected housing research institutions in the country, just released America’s Rental Housing 2026, its flagship biennial report on the state of rental housing in the United States.

The report is comprehensive and deeply valuable. But its operating cost analysis draws from Trepp, NCREIF, and MSCI, data sources that track professionally managed, commercially financed properties. The insurance doubling that Harvard documents, the 42 percent spike in material costs, the 24 percent increase in construction labor: those numbers are drawn from the institutional market. The small operator absorbing the same cost pressures with less negotiating power, thinner reserves, and no economies of scale is invisible in the research but very real in the market.

And there’s a reason these providers can offer housing that the market calls affordable. They generally live close to their units. They do the maintenance themselves, or with a very small crew. And critically, they bought these properties when prices were much lower, often at lower interest rates. Even when rates were high, as they were in the 1980s, the actual purchase price of the home was a fraction of what it would cost today, even adjusted for inflation. That cost basis is what allows the rent to stay low. It’s not charity, but the rents often do fit what federal programs like Section 8 can pay. It’s math that only works because the provider got in decades ago and stayed.

That math can’t be replicated by anyone entering the market today.

WHAT BREAKS THE ARC

The arc works because the economics, barely, stubbornly, precariously, still pencil. A provider can charge $950 a month, cover the mortgage, pay the insurance, handle routine maintenance, set aside something for capital expenses, and earn a modest return. Not the return that attracts institutional capital. But enough to keep going. Two things break it.

The first is mandates. Often framed as “protections,” these policies are frequently drafted by those completely disconnected from the operational realities of housing.

When a local government requires the installation of specific building systems in older structures, or caps the ability to recover costs, they are making politically expedient choices that shift the burden of the housing crisis directly onto the independent provider. The cost doesn’t land on an abstraction called “the landlord.” It lands on the person operating a 1960s building at $950 a month, whose insurance just doubled, whose property taxes just increased, and whose maintenance costs are up 40 percent since the pandemic. The provider faces a choice: absorb the cost and go unprofitable, pass it to the tenant and destroy affordability, or exit. Every path leads to the same place. The naturally occurring affordable unit ceases to exist. There is a physical limit to what can be retrofitted into an older building before the mandate becomes a renovation, and a renovation at today’s costs produces a unit that can no longer rent at yesterday’s price.

The second is eviction law that makes risk unmanageable. The ability to remove a tenant who doesn’t pay rent or who endangers other residents isn’t a luxury for the operator. It’s the structural framework that makes the whole enterprise viable.

When that enforcement mechanism becomes buried in bureaucratic delays, expensive legal hurdles, or is functionally outlawed, the small operator can’t price the risk. One non-paying tenant in a fourplex doesn’t reduce revenue by 25 percent. It can eliminate the entire margin and then some. Unlike an institutional owner with a legal department and a reserve fund, the NOAH provider absorbs that risk personally, and risks losing the tenants who are paying, the ones who leave because they don’t want to live around problems they didn’t create. People make decisions every day on far less consequential things than whether their building feels safe.

These two forces, mandates that raise the cost floor and enforcement uncertainty that removes the risk ceiling, create a distortion where nobody benefits. The tenant doesn’t benefit because the unit becomes more expensive or disappears. The provider doesn’t benefit because the operation becomes unprofitable. The community doesn’t benefit because the affordable housing stock shrinks. The only people who benefit are the ones who never lived in the building or operated it, the ones who wrote the policy and moved on.

WHAT WE LOSE

We are already seeing the fallout of these distortions. Harvard reports that 9.3 million units renting below $1,400 disappeared between 2014 and 2024, including 2.5 million renting under $600. Those weren’t public housing units demolished by the state. They weren’t tax credit properties aging out of compliance. They were NOAH units. They disappeared because the independent providers who operated them finally hit the wall where the math stopped working.

The trajectory is starkly divergent. Since 2019 alone, the number of cost-burdened renters has grown by 2.3 million while the supply of units renting below $1,400 has shrunk by millions. More people need affordable housing. Less of it exists. And the gap is widening because the providers who filled it are being pushed out.

But statistics don’t capture the actual casualty of this loss. When those units disappear, what is left with them is hard to fully measure on a spreadsheet. Culture is not something you can quantify. But you know it when you see it. It’s alive. You can feel it.

A neighborhood with affordable rentals is a neighborhood where the home health aide lives on the same block as the family she cares for. The cook at the restaurant on the corner walks to work. Where the retired widow on Social Security has lived for twenty years and knows everyone on her floor. Where the young couple saves for a down payment without drowning in rent, and when they buy their first house, it might be right there in the same neighborhood, because they already belong to it. In an era of remote work, renters have the freedom to try out neighborhoods and communities before committing. That exploration happens in rentals. It’s how people find where they belong.

These are people whose housing works because someone, somewhere, is operating a building at a price point the market would rather abandon.

And this is the difference that matters. Not “affordable” because a unit cost $650,000 to build and carries deed restrictions and layered subsidies and gets called “affordable” in a press release. Not “affordable” in the way that a tax credit project is affordable, where it costs more per unit than market-rate construction, but the tenant’s share is reduced through public financing. Those programs have a role. But they are not what houses most of America’s working renters.

What houses them is a home. A real one. One that became affordable because someone built it, and someone maintained it, and time made it modest, and a provider kept operating it because they could. Because math worked. Because they were part of the community too.

When that provider leaves, the home doesn’t become more affordable. It becomes more expensive, or it becomes nothing. And the community that grew up around it, the culture, the connections, the sense of place, goes with it.

The arc of affordable housing and the Ark from the Book are built the same way: not in a moment of crisis, but through the long discipline of doing the work before the flood arrives, for families and the future depend upon it.