What Our New TAX LAWS Mean For You

If you own a handful of rental properties in Washington, taxes probably aren’t your favorite topic—but they are one of the most important. Recent changes at both the state and federal level will affect how your rental business, your long-term planning, and even your legacy are taxed.

The good news? Most small housing providers won’t see immediate tax increases. The bigger impact is on planning, especially around estate taxes, capital gains, and high-income scenarios.

Let’s break down what’s changing and what it means in practical terms.

ESTATE TAXES: WASHINGTON STATE CHANGES (Effective July 1)

Washington continues to have one of the more aggressive estate tax systems in the country, and recent updates make planning even more important.

Fixed Exemption: $3 Million

Starting July 1, Washington’s estate tax exemption will be $3 million per person, and—importantly—it will not increase with inflation.

Last year’s law increased the exemption to $3 million AND allowed the exemption to rise over time. The automatic increases are gone.

Why it Matters:

If your total estate (including rental properties, your home, retirement accounts, and other assets) exceeds $3 million, your estate could owe tax when passed to heirs.

For many small housing providers, this threshold is easier to hit than it sounds. A couple of appreciated properties plus a primary residence can quickly push you over the limit.

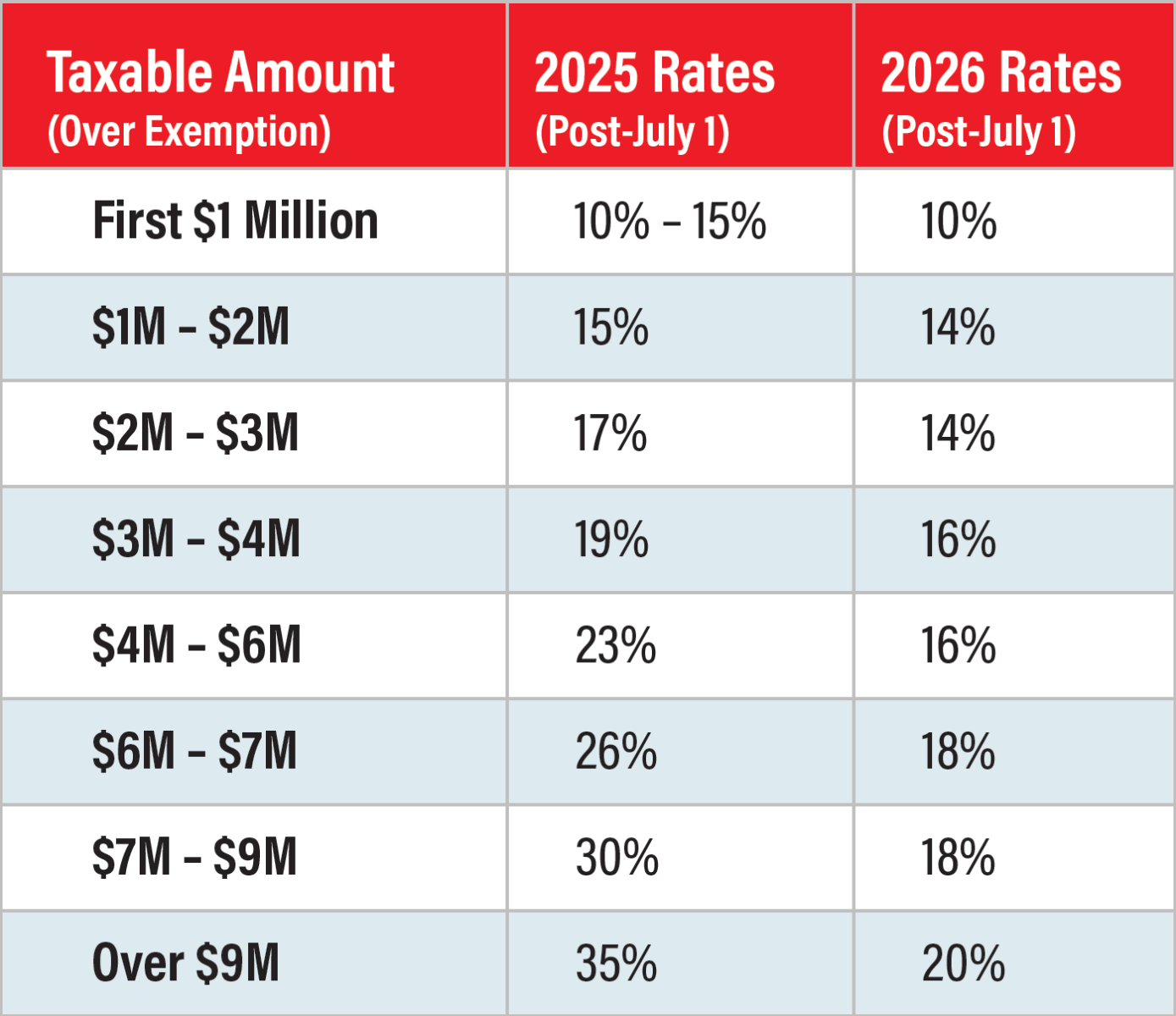

Tax Rates Reset (10% to 20%)

The state is reverting to a 10%–20% estate tax rate structure, down from last year’s temporary higher rates (which capped at 35%).

Why it Matters:

While the exemption is relatively low, the tax rates themselves are now more moderate than in 2025.

WA State Estate Tax Rates Comparison Table Individuals with estate valued at less than $3 million are exempt.

No Portability Between Spouses

Washington still does not allow “spousal portability.”

What that Means:

If one spouse dies and doesn’t fully use their $3 million exemption, the unused portion cannot be transferred to the surviving spouse.

Why it Matters for Housing Providers:

Married couples with rental portfolios need to plan carefully. Without proper structuring (like trusts), you could unintentionally lose part of your combined exemption.

Still No Washington Gift Tax

Washington continues to not impose a gift tax.

Why it Matters:

You can transfer assets (including partial interests in rental properties) during your lifetime without triggering a state-level gift tax.

This opens the door to strategic estate planning, such as gradually transferring ownership to children or heirs. However, it is important to be careful when gifting assets with a low tax basis, as that basis will pass on to children.

FEDERAL ESTATE & GIFT TAX UPDATES (Effective January 1)

At the federal level, the estate tax rules are much more forgiving—but still worth understanding.

Higher Federal Estate Tax Exemption: $15 Million Per Person

The federal exemption is now $15 million per individual, or $30 million for married couples.

Why it Matters:

You are far less likely to owe federal estate tax, even with multiple properties.

However, this high exemption isn’t guaranteed forever. It has changed multiple times over the years and could drop in the future.

Federal Estate Tax Rates: 18% to 40%

If your estate exceeds the exemption, federal estate tax rates range from 18% up to 40%.

For most small housing providers, this is more of a long-term planning consideration than an immediate concern.

Annual Gift Exclusion: $19,000

You can gift up to $19,000 per person per year without triggering federal gift tax reporting requirements.

Note that you can always gift more but just need to report the gift.

Example:

- $19,000 each to a child

- For a total of $38,000 per year per child

Why it Matters:

This is a powerful tool for gradually transferring wealth, especially if your rental portfolio is growing in value.

WASHINGTON’S NEW “MILLIONAIRE’S TAX” (Effective January 1, 2028)

Washington is also introducing a new high-income tax aimed at top earners.

9.9% Tax on Income Over $1 Million

Starting in 2028, individuals earning more than $1 million annually will pay a 9.9% tax on income above that threshold.

This includes:

- Wages

- Business income

- Rental income

- Capital gains

- Stock dividends

- Interest

Credits to Prevent Double Taxation

The law includes credits for:

- Existing Washington capital gains tax

- Out-of-state income taxes

- B&O (Business & Occupation) taxes

Why it Matters:

These credits help reduce the risk of being taxed multiple times on the same income—but they won’t eliminate the tax entirely for high earners.

Exemptions for Property Sales and Some Small Businesses

Luckily, the sale of real property is specifically exempt from the tax since the state already issues an excise tax on these sales.

There are limited exemptions for certain small, family-owned businesses. Whether your rental activity qualifies will depend on how your business is structured and how the final rules are interpreted.

This is an area to watch closely as guidance develops.

Increased B&O Exemption

The law also raises the B&O tax exemption threshold, which could benefit smaller business operators.

Why it Matters:

If your rental-related business activities fall under B&O taxation (short-term rentals), you may see some relief at lower income levels.

WHAT THIS MEANS FOR SMALL HOUSING PROVIDERS

Let’s bring it all together in practical terms.

Most Housing Providers Won’t See Immediate Tax Increases

If you:

- Own a few properties

- Earn well under $1 million annually

- Have a total estate under $3 million

…these changes may not affect your taxes right away.

But Estate Planning Just Became More Important

The $3 million Washington estate tax threshold is the biggest issue for many housing providers.

Real estate appreciation alone can push you over that limit—even if your cash flow is modest.

Key Takeaway:

If you plan to pass your rentals to family, you should be thinking about:

- Ownership structure

- Trusts

- Gifting strategies

PRACTICAL NEXT STEPS

You don’t need to overhaul everything—but you shouldn’t ignore these changes either.

Consider:

- Reviewing your net worth

Include property values, not just income. - Talking with an estate planning attorney

Especially if you’re near or above $3 million in total assets. - Evaluating ownership structure

LLCs, partnerships, and trusts can play a role. - Planning asset sales strategically

Timing could matter more after 2028.

FINAL THOUGHTS

For Washington’s small housing providers, the story isn’t about sudden tax hikes—it’s about quiet thresholds that sneak up on you.

A couple of well-performing rentals bought years ago can now represent a significant estate. With the exemption set at $3 million and not rising, more families will find themselves affected over time.

The earlier you plan, the more options you have—and the less likely your hard-earned properties will create unintended tax burdens for the next generation.

Julie Martiniello is a Co-Owner and Managing Partner at Dimension Law Group, where she focuses on Estate Planning, Probate, Real Estate, and Business Law, helping business owners, real estate investors, and families protect their assets and plan for the future. She may be contacted via julie@dimensionlaw.com. Visit their website dimensionlaw.com.