LEVIATHAN: Washington’s Proposed Income Tax & Its Effects on Housing Abundance

“As nightfall does not come at once, neither does oppression. In both instances, there is a twilight when everything remains seemingly unchanged. And it is in such twilight that we all must be most aware of change in the air—however slight—lest we become unwitting victims of the darkness.”

— Justice William O. Douglas (raised in Yakima, WA)

The Rental Housing Association of Washington exists to support the providers who house our state, to advocate for policies that expand housing supply, and to ensure that rental housing remains viable for independent owners and operators.

Housing abundance, more homes, better-maintained homes, and sustained private investment—is not an abstract goal. It is the only durable path to housing stability.

However, Washington’s proposed 9.9 percent income tax introduces a “twilight” of structural risk that directly undermines this stability. While often described as a “tax on millionaires,” the design of the policy reveals a framework misaligned with the economic realities of rental housing.

By importing federal income definitions, aggregating household income, taxing undistributed pass-through earnings, and increasing compliance exposure, the proposal increases risk in a sector that already operates on thin margins and long planning horizons. The result is not theoretical. It is reduced reinvestment, slower supply growth, market consolidation, and increased pressure on tenants over time.

A NOTE ON FUTURE RISK: TODAY’S BILL IS TOMORROW’S BASELINE

Important: The figures in this analysis—including the 9.9% rate and the $1 million threshold—are based on the current legislative text. However, these figures are statutory, not constitutional. They can be revised by a simple majority vote in any future legislative session.

Crucially, this tax does not take effect until January 1, 2028, with revenue not expected until 2029. It does nothing to address Washington’s current budget shortfalls or the deficit projected for the immediate future.

This reveals the true nature of the proposal. It is not an emergency measure to fix a hole in the budget; it is a structural expansion of the state itself. This is the Leviathan in motion: a government apparatus establishing a permanent, potent new revenue stream not to pay for what it has done, but to clear the path for what it intends to become. By the time the revenue arrives in 2029, the state’s spending baseline will have already risen to meet it, requiring the cycle—and likely the tax rates—to expand once again.

UNDERSTANDING THE MECHANICS

While the headline is the 9.9% rate, the impact lies in the technical structure of the tax. RHAWA’s analysis of the legislative proposal highlights several key mechanisms that every housing provider must understand:

- The Rate & Base: A 9.9% tax is imposed on “Washington taxable income,” defined broadly by reference to federal Adjusted Gross Income (AGI).

- The Deduction: A standard deduction of $1,000,000 is established. While indexed for inflation, for married couples and domestic partners, the deduction is capped at $1,000,000 combined. This creates a disparity compared to two unmarried individuals, who would each receive their own $1 million deduction (see “Marriage Penalty” below).

- No Independent WA Loss Carryforwards: Crucially, the proposal diverges from federal tax principles by prohibiting any independent Washington-specific carryforward of losses. Unless a loss qualifies as a Federal Net Operating Loss (NOL) that reduces your future federal AGI, the “Washington” portion of that loss effectively disappears.

- Credit Limitations: Credits for taxes paid to other jurisdictions or B&O taxes are restricted—they are non-refundable and cannot be carried forward or backward.

- Administration: The Department of Revenue is granted broad authority to administer the tax, including requirements for quarterly estimated payments and audit powers similar to existing business taxes.

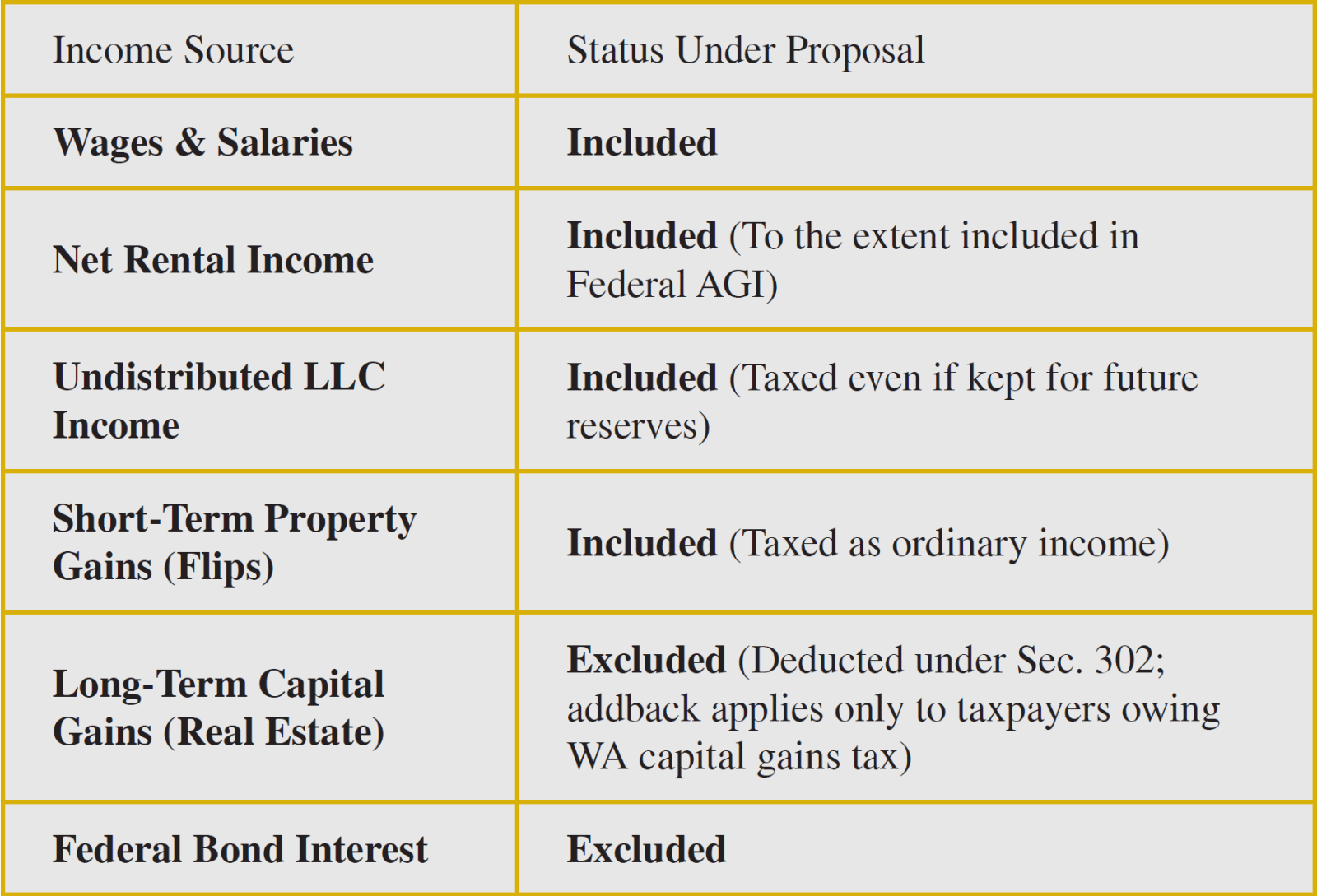

WHAT COUNTS AS INCOME—AND WHY HOUSING IS AFFECTED

Because the proposal uses federal AGI as the starting point, the taxable base includes wages, salaries, net business income, and net rental income (to the extent included in federal AGI).

For rental housing providers, the treatment of pass-through entities is decisive. Most rental housing in Washington is owned through LLCs, partnerships, or S corporations. Under the proposed structure, owners are taxed on their pro-rata share of the entity’s income.

Crucially, “pass-through income” is defined to include both distributed and undistributed federal taxable income. This means providers will face tax liabilities on net income that has not been cashed out, but instead retained in the business for future reserves, capital improvements, or debt service covenants.

This increases the likelihood that providers face new tax obligations in years when liquidity is constrained. In effect, the tax hits reinvestment capital before it can be deployed to maintain housing quality.

Sidebar: Does It Count as “Washington Taxable Income”?

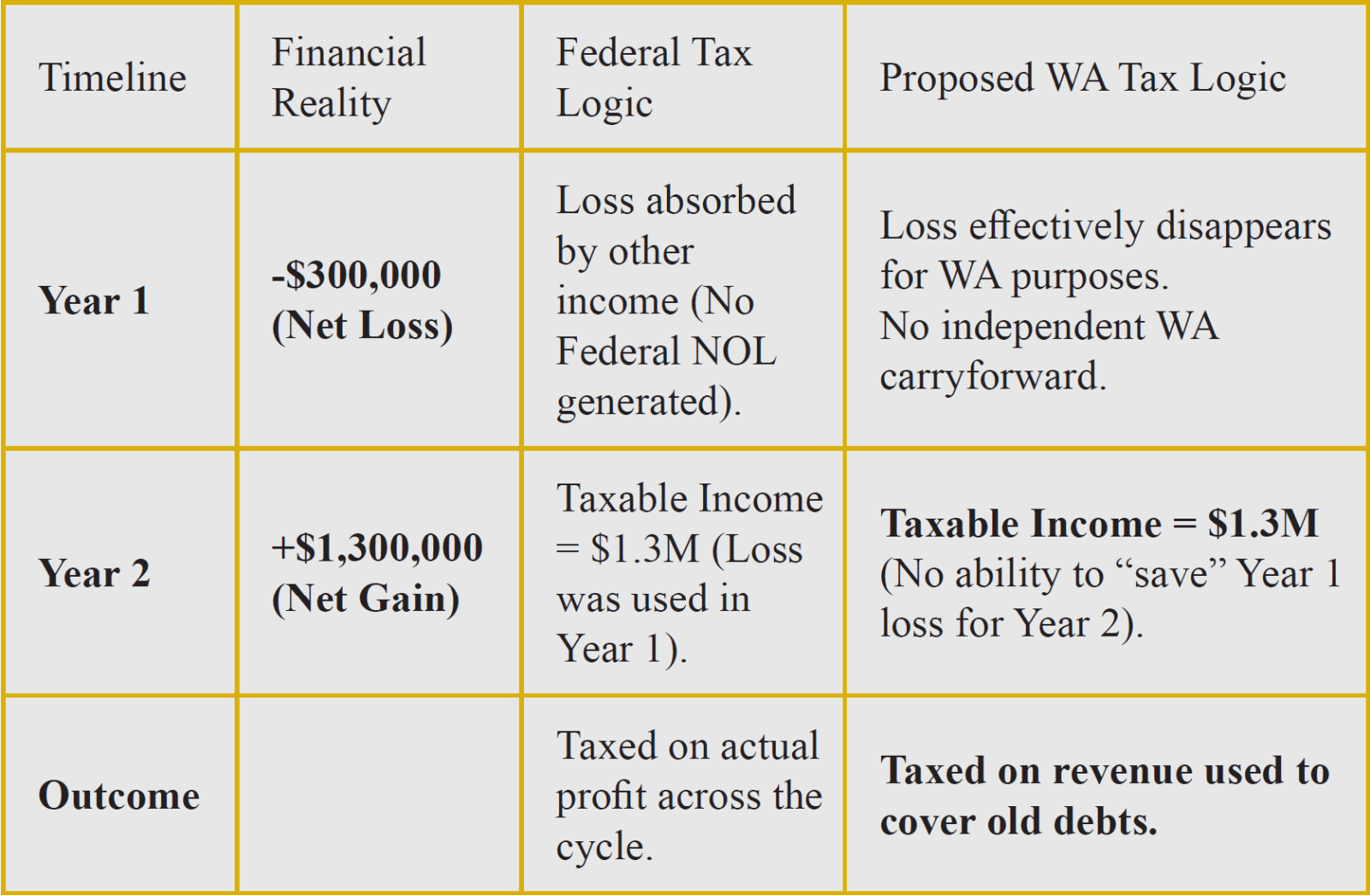

THE “HOUSING CYCLE PENALTY”: A CASE STUDY

To understand why the lack of independent loss carryforwards is so damaging to housing, consider the following common scenario for a mid-sized housing provider who incurs a loss during a major renovation year.

Scenario: A provider spends heavily on repairs in Year 1, resulting in a net loss that is absorbed by other income (e.g., a spouse's W-2 wages) on their joint federal return, leaving no Federal Net Operating Loss (NOL) to carry forward.

The Result: The state taxes the recovery while ignoring the cost of the maintenance. This structure penalizes providers for making necessary capital improvements, incentivizing deferred maintenance and degrading the quality of housing stock over time.

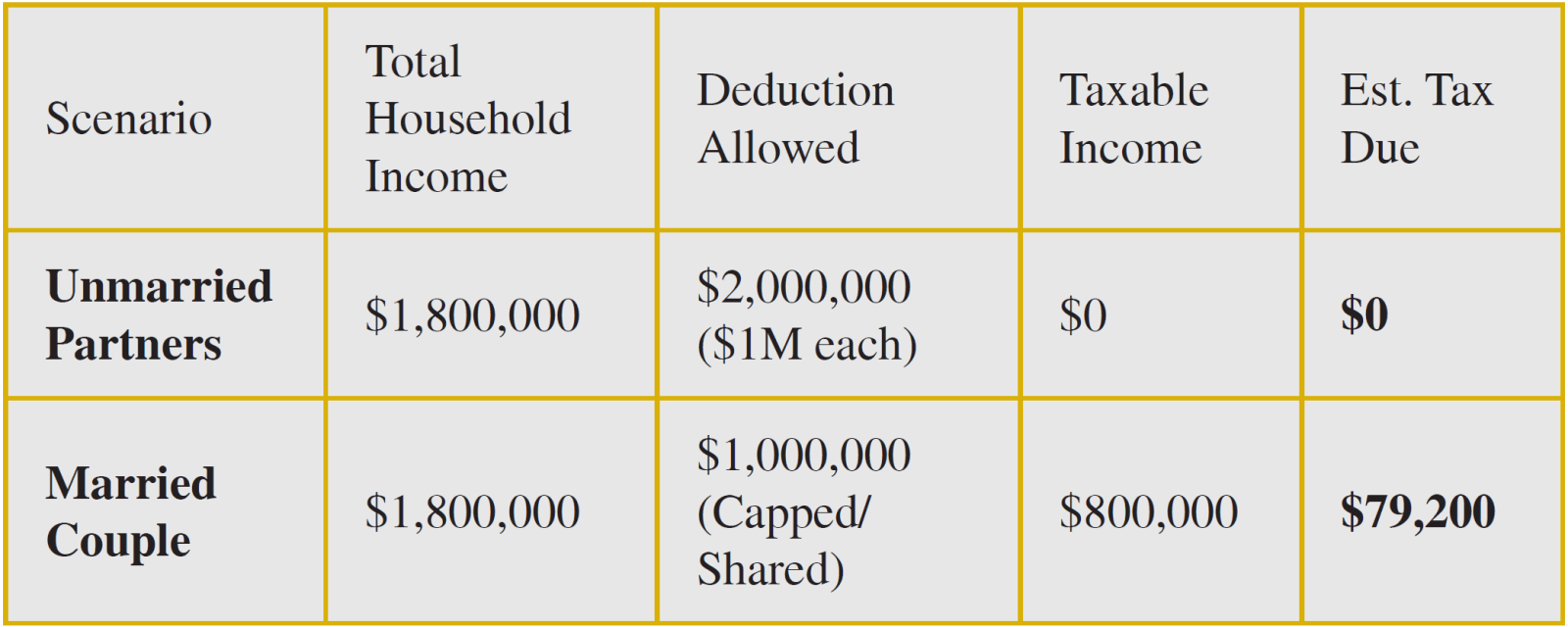

HOUSEHOLD AGGREGATION AND THE MARRIAGE PENALTY

The proposal aggregates income at the household level. Rental income is combined with wage or business income earned by a spouse or partner, and the shared deduction applies regardless of the income source. This aggregation creates a stark disadvantage for family-run businesses compared to unmarried partners or corporate structures.

Table: The Marriage Penalty Impact - Scenario: Two household leaders running the exact same business with $1.8M total net income.

This penalty creates an arbitrary cost for family ownership, often the backbone of naturally occurring affordable housing in Washington.

WHY THIS MATTERS BEYOND “HIGH EARNERS”

Housing markets transmit cost and risk. Taxes imposed at the ownership and capital level do not stay there; they shape market behavior. When housing providers face higher and less predictable tax exposure, predictable behavioral responses follow:

- Capital is diverted from property upgrades toward tax compliance and reserves.

- Marginal providers—particularly smaller operators unable to absorb the administrative complexity of apportionment rules—exit the market.

- Ownership consolidates toward larger entities better positioned to manage compliance and overhead.

- Out-of-State Impact: It is worth noting that this tax applies to income derived from Washington property regardless of where the owner lives. This impacts the out-of-state investment capital that Washington relies on to build and maintain its housing supply.

Over time, these dynamics constrain supply and reduce flexibility, placing upward pressure on rents and reducing choices for tenants—including households that will never approach the statutory income threshold.

WHY TENANTS SHOULD OPPOSE THIS PROPOSAL

Tenants are often told that taxes on housing providers will not affect them. In reality, rental housing markets transmit cost, risk, and constraint directly to renters. When a policy increases the volatility and cost of providing housing, tenants experience the consequences first.

This proposal raises the cost of operating rental housing in ways that reduce reinvestment, slow new supply, and narrow the range of housing options available to renters. As providers divert capital toward tax compliance and reserves—or exit the market altogether—fewer homes are built, fewer upgrades are made, and fewer units remain available at any given price point.

Over time, this has predictable effects. Renters face tighter vacancy rates, reduced bargaining power, and fewer choices. Housing providers become less flexible when working with tenants during periods of hardship, because higher fixed costs leave less room to absorb risk. Deferred maintenance becomes more common as reinvestment is penalized, degrading housing quality and tenant experience.

THE "PUBLIC SAFETY" ILLUSION

Notably, approximately 95% of the projected revenue from this tax flows into the state’s General Fund, with a remaining 5% directed toward a new prosecutor and county public safety account. While framed as targeted investment in safety, Washington’s budget structure allows funds to be shifted freely between categories. This design creates a political narrative around "law and order" to shield the tax from criticism, while functionally doing little more than expanding the General Fund's capacity to absorb new spending.

Importantly, these effects fall hardest on moderate-income renters—not high earners. Tenants seeking naturally occurring affordable housing, older units, or smallscale rental properties are the most exposed when small and mid-sized providers exit, and ownership consolidates into fewer, larger operators.

In a housing-constrained market, policies that reduce supply and reinvestment do not create affordability. They do the opposite. They increase competition for fewer homes and shift costs downstream to the people who rely on the rental market the most. Tenants need more homes, more choice, and more stable housing providers. This proposal moves the market in the opposite direction.

WHO IS MOST IMPACTED BY THIS PROPOSAL?

HB 2724 / SB 6346 does not hit all housing providers evenly. Its structure specifically targets the operational models most common among local, mid-sized housing providers—the very people who maintain the bulk of Washington’s naturally occurring affordable housing.

Based on the bill’s definitions of income, deductions, and loss carry forwards, these are the profiles most exposed to the new tax:

-

The “Prudent” Operator (Small & Mid-Sized LLCs)

• Profile: An owner of a 20-unit building in Spokane who keeps $200,000 in the LLC bank account to save for a future roof replacement or unexpected vacancy.

• The Hit: Because the proposal taxes undistributed pass-through income, this owner is taxed on that $200,000 as if it were personal salary, even though they cannot spend it. They face a cash tax liability on “phantom income” that is legally trapped in the business for safety and maintenance.

-

The Married “Mom-and-Pop” (Family-Run Businesses)

• Profile: A married couple with W-2 day jobs who manage a small portfolio of rentals on the side.

• The Hit: The shared $1,000,000 deduction cap for married couples creates a structural disadvantage for family businesses. This couple reaches the tax threshold twice as fast as two unmarried business partners with the exact same income, effectively facing a marriage penalty for running a housing business together.

-

The “Turnaround” Specialist (Rehabbers)

• Profile: An investor who buys a dilapidated duplex, incurs a heavy repair loss in Year 1 (which they offset against their other W-2 income on their federal return), and stabilizes it in Year 2.

• The Hit: Because the Year 1 loss was used federally, there is no Federal NOL to carry forward. Since the bill prohibits carrying forward Washington-specific losses, the owner pays zero tax in the bad year but pays full tax on the Year 2 “recovery” income. The state taxes the revenue recovery while ignoring the startup costs that made it possible.

-

The Short-Term Developer

• Profile: An investor or builder who constructs or renovates housing for sale (merchant building).

• The Hit: Unlike long-term holders who can deduct long-term capital gains from the tax base, those with short-term gains or ordinary business income from development are fully exposed to the 9.9% rate. This subtly punishes the active creation of new housing supply while sheltering passive holding.

-

Self-Managing Providers Who Do Not “Pay Themselves”

• Profile: Owners who do not take regular distributions or salaries, preferring to let earnings sit in the business to maintain liquidity and property quality.

• The Hit: Under this proposal, they are taxed on that retained income regardless of whether they ever personally receive it.

-

Out-of-State Investors Who Own Washington Property

• The Hit: Income derived from Washington real estate is allocated to Washington regardless of where the owner resides. This directly affects the national investment capital that Washington relies on to purchase, rehabilitate, and maintain its housing stock.

Who is Safe? Conversely, the tax structure largely exempts two groups:

- Long-Term Holders: Owners who simply hold property for appreciation and sell after one year are generally exempt from this specific tax on the sale proceeds (due to the deduction for long-term capital gains and the real estate exemption in the add back rules).

- Institutional Giants: Large C-Corporations and REITs do not pass income through to individuals in the same way, often shielding them from the personal income tax mechanisms designed in this bill.

RHAWA’s Position

RHAWA is unequivocally pro-housing. We support policies that expand supply, encourage reinvestment, and preserve a diverse ecosystem of housing providers—from small, independent owners to larger operators capable of building at scale.

A tax framework that broadly imports federal income definitions, taxes undistributed pass-through income, aggregates household income, and increases compliance exposure directly goes against those goals. It penalizes reinvestment, accelerates consolidation, and reduces the long-term production and maintenance of housing.

Washington needs more homes. This proposal will not build them. It will set in motion the slow-moving Leviathan described at the outset, one that grows quietly in structure while the conditions for housing abundance steadily recede.